What are the 9 best investments in the UAE for Expats?

The United Arab Emirates (UAE) is a magnet for expatriate investors, and it’s easy to see why. Nearly 88.5% of the UAE’s 11.5 million residents are expats, drawn by a safe, high-quality lifestyle and strong economic opportunities.

The country’s tax-free investment environment and strong financial markets make it an attractive place to invest and boost returns.

But with so many investment choices like property, stocks, gold, savings plans, global platforms, and crypto, it’s easy to feel overwhelmed or take the wrong advice.

This guide simplifies everything for you. By the end of this guide, you will know what’s the best investment in the UAE for expats, the estimated ROI, and several other details related to investments in the UAE.

Why invest?

Keeping your savings in a traditional bank account won't cut it. Inflation can quietly erode your purchasing power.

Globally, inflation has averaged around 2% annually since 1999, which is the target for many central banks, including the European Central Bank.

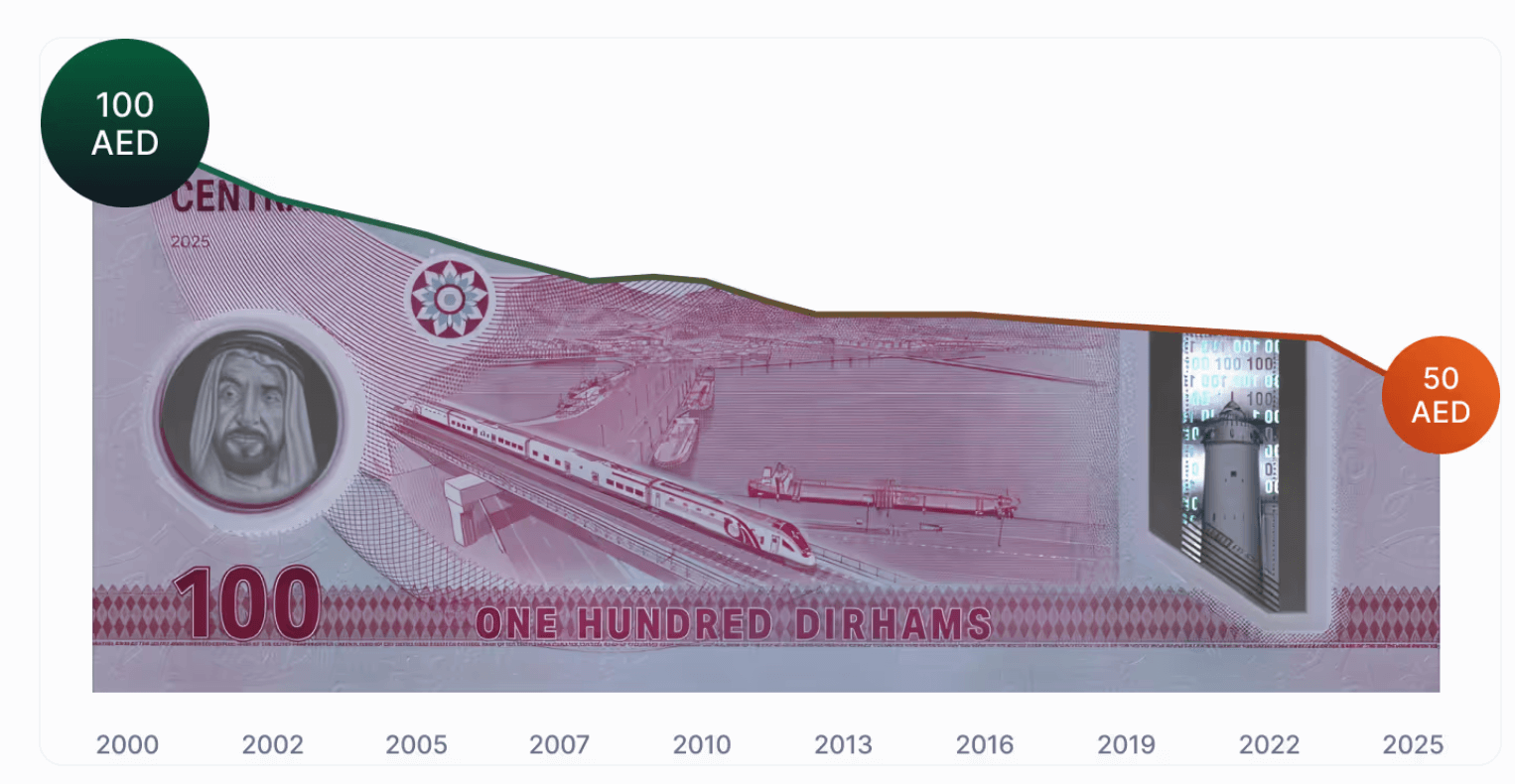

Based on the UAE consumer price inflation, 100 AED in 2000 was only worth only 50 AED in 2025. This means a continuous, subtle loss of purchasing power over time, as you can see from the image below:

Representation based on UAE consumer price inflation (2000–2025). Data from IMF/World Bank statistics.

The great news is that in the UAE, you have numerous avenues to make your money work for you, even if you start with small amounts.

Curious to see how your money can grow over time thanks to compound interest?

Try our Compound Interest Calculator to visualize how small, consistent investments can turn into long-term wealth.

Top investments in the UAE for Expats

To help you navigate the options, here’s a summary of the 9 best investments for UAE expats.

| Investment | Estimated ROI (Annual) | Liquidity | Risk Level |

|---|---|---|---|

| Real estate | 5% to 9% (rental yield) | Low: illiquid asset | Medium |

| Global shares and ETFs | 6% to 10% (historical) | High: daily trading | Medium |

| UAE stock market | 3% to 6% (plus dividends) | Medium: local exchanges | Medium |

| Gold | 4% to 6% (long-term) | High: physical/ETF | Medium |

| Bonds (Sukuk) | 3% to 5% (yield) | Medium | Low to Medium |

| High-yield savings account |

AED rates: 3% to 4.5% USD rates: 4.5% to 5.5% (interest) |

High: on-demand | Low |

| Mutual funds & robo-advisors | 5% to 8% (balanced port.) | High: sell anytime | Medium |

| Cryptocurrencies | -100% to +100% (very volatile) | High: 24/7 market | High |

| Startups/Private equity | 0% to 30%+ (highly variable) | Low: years to exit | High |

Note: “Liquidity” means how easily you can turn an investment into cash - for example, a savings account is highly liquid, while real estate is not. The returns shown are only estimates; past performance is not a guarantee of future results.

Now, let’s dive into each investment option in depth and know which ones are the perfect fit for you.

1. Real estate

Best for: Expats seeking steady rental income, long-term capital growth, and asset-backed stability in Dubai or Abu Dhabi.

Real estate is one of the most popular ways for expats to invest in the UAE due to strong rental demand, clear regulations, and good returns.

Dubai and Abu Dhabi offer the highest opportunities, especially in freehold communities where foreigners can fully own property and receive a title deed.

There are the main types of real estate you can invest in:

- Residential: Apartments in areas like Dubai Marina, Business Bay, Downtown Dubai, and Abu Dhabi’s Yas Island often deliver 7 to 9% rental yields. Villas yield slightly lower returns, around 4-6%.

- Commercial: Offices, warehouses, and retail units can generate higher rental income, but vacancy and resale risk are also higher.

- Off-plan: Under-construction projects usually offer lower entry prices and attractive payment plans, offering better capital appreciation potential if bought early.

Expats can buy freehold property in designated zones, giving full ownership and a title deed from the Dubai Land Department.

Leasehold options, more common in parts of Abu Dhabi and Sharjah, offer rights for up to 99 years but not land ownership. While leasehold may have lower entry costs, freehold offers more substantial long-term value and security. Depending on location and property type, you can expect an annual ROI of 5% to 9%, combining rental yields and potential price appreciation. Be aware that this value is indicative only.

Dubai remains one of the leading global cities for rental income. In the H1 of 2025, total real estate sales in Dubai alone reached AED 431 billion.

Real estate is a solid long-term investment, but it requires a higher entry capital and is less liquid. Expats who want exposure without owning property directly can explore REITs or regulated real estate crowdfunding platforms like Stake (feel free to check our Stake review).

2. Global shares and ETFs

Best for: Expats wanting diversified global growth across international markets, with USD trading currency that aligns with the AED-USD peg.

For UAE expats, investing in global stocks and ETFs offers access to international growth while diversifying beyond the local market.

Platforms like Interactive Brokers, Swissquote, and eToro allow you to invest in US, European, and Asian markets from the UAE.

If you prefer a local presence, Sarwa Trade offers a beginner-friendly, ADGM-regulated app with fractional investing and low minimums.

Want to know how you can invest in global shares and ETFs? Read our other guides to know more:

- Best ETFs to invest in from the UAE

- How to invest in US stocks from the UAE

- Best trading apps in the UAE

- How to invest in the S&P 500 from the UAE

ETFs are quite popular in the UAE, and expats are investing actively in them. As of Q1 2025, Exchange-traded funds (ETFs) saw their market value more than double, rising 109% to approximately AED 1.64 billion, compared with AED 784.4 million in Q1 2024.

Popular ETFs include:

- S&P 500 ETFs like CSPX (USD-denominated UCITS, ISIN IE00B5BMR087) for non-Americans, or IVV for US persons

- Global funds like Vanguard FTSE All-World (VWRA, USD) covering 3,600+ developed and emerging market stocks

- Sector-specific ETFs in tech, healthcare, and emerging markets

For a deeper look at UAE-friendly ETF picks aligned with the AED-USD peg, see our guide on the best ETFs to invest in from the UAE.

These funds trade like stocks, are highly liquid, and typically charge low annual fees (0.1% to 0.3%).

Most platforms let you fund your account via UAE bank transfers or cards.

Returns on a global ETF portfolio can average 7% to 10% annually over the long term, but volatility is part of the journey. We recommend you start with small amounts and build gradually.

Want to see how investing in the S&P 500 could have performed over time? Use our S&P 500 Calculator to simulate potential future returns.

According to the UBS Global Investment Returns Yearbook (published by Credit Suisse until 2023, by UBS since), 126 years of data show that since 1900, equities have outperformed bonds, bills and inflation across all countries with continuous histories. The headline long-run figures, in real (inflation-adjusted) terms:

- Stocks: ~5% real annual return

- Bonds: ~2% real annual return

However, keep in mind that there is a relationship between risk and return. In other words, stocks carry a higher risk (volatility) compared to bonds.

Please note that many UAE investors prefer Irish-domiciled UCITS ETFs to reduce U.S. tax exposure, by avoiding:

- A 30% withholding tax on U.S. dividends (standard for non-U.S. investors).

- A U.S. estate tax above $60,000 in U.S.-domiciled assets. This applies only if you die and have more than $60,000 in US assets.

Want to learn more? Check this video, explaining how to invest in the S&P 500 from the UAE:

3. UAE stock market

Best for: Expats looking to tap into local economic growth, earn dividends, and stay close to home with familiar names.

The UAE’s stock exchanges: Abu Dhabi Securities Exchange (ADX), Dubai Financial Market (DFM), and Nasdaq Dubai, give you a way to invest directly in the region’s growth.

ADX and DFM list major domestic firms, while Nasdaq Dubai includes global and regional listings like Sukuk and REITs.

Expats can invest by first getting an Investor Number (NIN) from the relevant exchange, then opening a trading account with a local broker such as ADCB Securities, Emirates NBD Securities, or online platforms like eToro. Most brokers support AED transfers and offer direct access to listed UAE stocks.

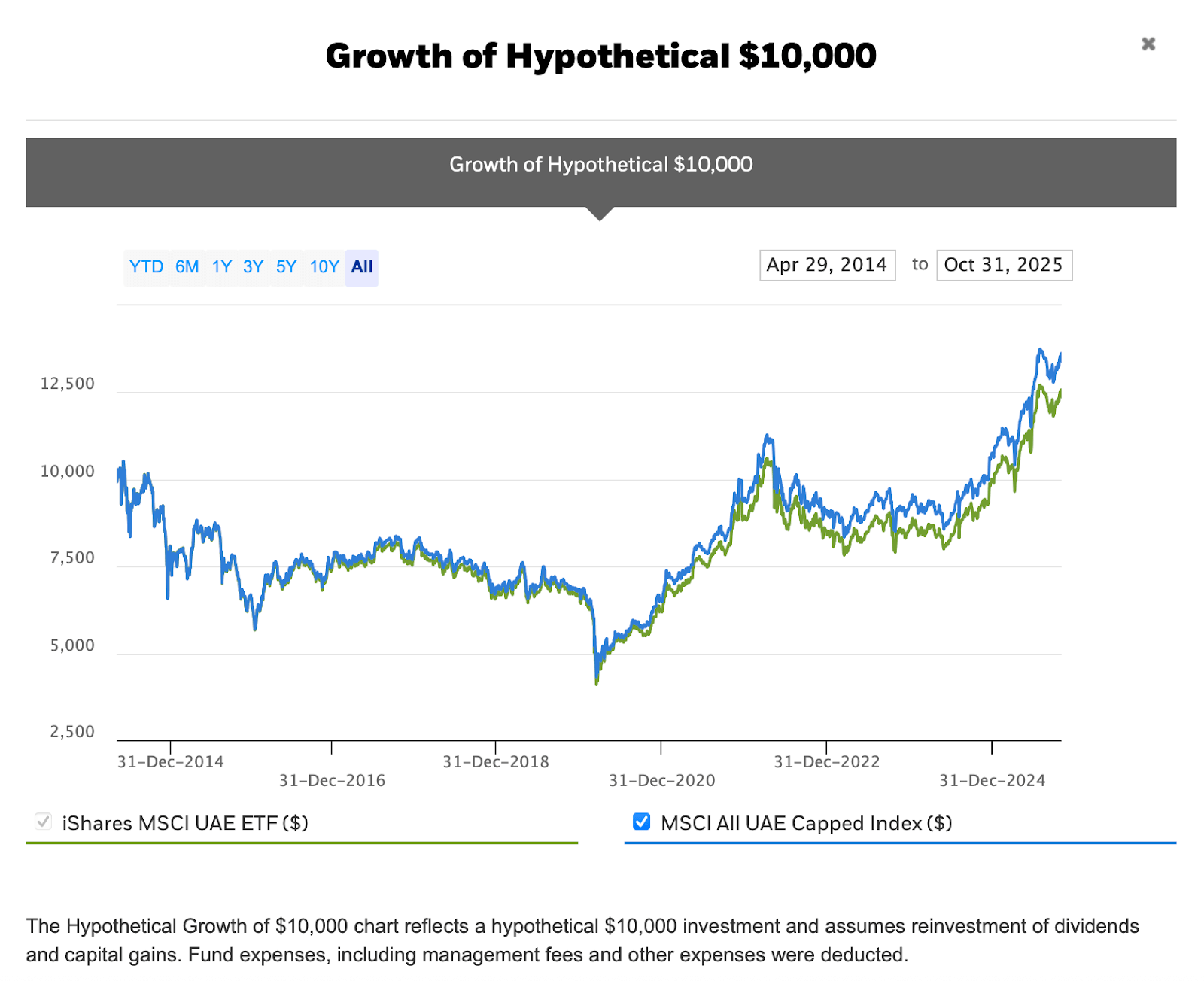

Those seeking diversification can consider the iShares MSCI UAE ETF, an ETF that tracks the UAE market, which holds major names like Emaar, ADNOC, and Aramex.

Since its inception in 2014, the fund has reflected the long-term development of the UAE’s equity markets, with calendar year NAV returns of +44.10% (2021), -5.31% (2022), +2.91% (2023), +15.26% (2024), and +21.61% (2025). The fund tracks the MSCI All UAE Capped Index but tends to lag slightly due to expenses and tracking differences.

The chart below illustrates this performance over time, showing both the ETF’s evolution and its benchmark comparison:

The market has lagged global peers like the S&P 500; however, past performance is not indicative of future results.

Also read: 8 best stock brokers in the UAE (local + global)

Want to learn how to do it step-by-step? Check out this video, explaining how to invest in the UAE stock market:

4. Gold

Best for: Cautious expats looking for a stable, tax-free hedge against inflation and market volatility.

Gold remains a popular investment for UAE expats, offering both safety and liquidity. Dubai, known as the “City of Gold,” has long been a major global trading hub, with tax-free access to physical and digital gold.

Physical gold can be bought easily through DMCC-certified dealers or the Gold Souk. While physical gold gives direct ownership, storage and resale require planning, especially as dealers charge a small premium over spot price. For simpler exposure, many expats prefer digital options:

- Gold ETFs like SPDR Gold Shares (GLD) or iShares Gold Trust track the gold price and trade on global exchanges. You can buy them through brokers like Swissquote, Interactive Brokers, or Sarwa.

- Gold accounts offered by UAE banks let you buy and sell gold grams through your mobile banking app, with the bank holding custody.

One of the biggest advantages? No tax on gold gains or capital repatriation. Liquidity is strong, especially in Dubai’s DMCC free zone, and the market is tightly regulated.

Gold typically returns 5% to 6% annually over the long run but fluctuates. It shines during market volatility or when the dollar weakens, but long-term growth is modest.

From 1978 to January 2025, gold recorded an approximate average annual return of 6.13%. However, this figure was just over half of the annual return of global stocks during the same period.

In other words, if you had chosen to keep an investment in gold over that period, you could have seen your purchasing power decline.

Also read: Best gold trading platforms in the UAE

5. Bonds (including Sukuk)

Best for: Income-focused expats who want predictable returns and low-to-moderate risk, especially through Sharia-compliant options.

Bonds are a solid option for expats seeking stable income with low to moderate risk. You can invest in both conventional bonds (which pay fixed interest) and Sukuk, which are Sharia-compliant and offer profit-sharing returns tied to assets, not interest.

Typical yields:

- UAE government Sukuk: ~4%

- Corporate bonds: 5% to 7%, depending on risk

Access options:

- Retail Sukuk is available through banks such as Emirates NBD and ADIB, with low minimums (as low as AED 1,000).

- Bond ETFs and mutual funds (like Franklin Templeton MENA Bond Fund) offer diversified exposure with lower entry points.

- Global bonds can be purchased through platforms like Swissquote or Interactive Brokers, including US Treasuries and emerging market debt.

Sukuk dominates the UAE market due to Islamic finance norms, but both Sukuk and global options function similarly from an investor’s perspective, paying regular income and returning principal at maturity. UAE sovereign bonds and high-grade corporate issuers are generally considered low-risk.

Holding individual bonds to maturity preserves capital, but early selling can lead to losses if interest rates rise.

Most importantly, the UAE has no personal tax on bond income, making it more efficient than some overseas options.

6. High-yield savings accounts

Best for: Expats prioritizing safety, liquidity, and steady interest income while keeping emergency funds intact.

For UAE expats looking for safety and returns, high-yield savings accounts (HYSAs) are a smart option. With rates between 3%-4.5% for AED and 4.5%-5.5% for USD, they’re ideal for emergency funds or short-term savings without market risk.

Here are some of the top UAE banks offering strong rates:

- Mashreq NEO PLUS Saver: 6.25% p.a. if salary is transferred to the account, or 5% p.a. if no salary transfer but you maintain AED 50,000+ monthly average balance.

- FAB iSave: 4.00% p.a. on new funds (campaign valid until March 31, 2026), with no minimum balance. Non-campaign balances earn the prevailing tiered rate (up to ~3.25% p.a.).

- ADCB Super Saver: Up to 4.5%, but needs AED 50,000+.

- Digital banks like Wio and Liv.: Offer 3.5% to 4.5% depending on savings goals or tenure.

Want to see more? Check out our article comparing the best high-yield savings accounts available in the UAE.

These accounts beat regular savings rates (often <1%) but come with conditions like minimum balance, new funds, or withdrawal limits.

If you’re an Expat sending money abroad, know this:

- Consider holding some savings in USD, GBP, or EUR, depending on future needs

- Watch out for high currency conversion fees when repatriating funds

- Use exchange houses or fintech apps for cheaper international transfers

7. Robo-advisors

Best for: Busy expats building wealth steadily, without getting caught in day-to-day market swings.

For expats who prefer a hands-off approach, robo-advisors like Sarwa, StashAway, and Wahed offer low-cost, diversified portfolios using global ETFs. You select a risk level, and the platform does the rest: rebalancing, monitoring, and adjusting over time.

- Sarwa (FSRA/ADGM-regulated): Invests in low-fee ETFs like Vanguard and iShares. It has expected returns of 5% to 8% per year on average for balanced portfolios. Sarwa Invest has tiered annual fees: 0.85% (Standard, under $100k), 0.7% (Platinum, $100k-$500k), and 0.5% (higher tiers), with a $7/month minimum charge that meaningfully increases the effective fee for small accounts. Minimum to start investing is $500.

- StashAway: Uses dynamic allocation, with ~0.8% fees and strong digital tools. Its cash management feature pays nearly 4%.

- Wahed: A Sharia-compliant platform investing in Halal ETFs, Sukuk, and gold. Good for ethical investors.

You can start with as little as AED 500 per month. Most platforms are locally licensed (DFSA or ADGM) and offer full transparency. Compared to traditional bank mutual funds, which often come with high fees and restrictions, robo-advisors are simpler, cheaper, and more accessible.

Returns vary by portfolio type: conservative portfolios may yield 3% to 5%, while aggressive ones target 7% to 10% long-term.

Robo-advisors are best for beginners who don’t want the hassle of having to choose which ETFs to buy, placing the trades, etc. On the downside, they come with a higher fee (generally an annual management fee).

The UAE has pretty great solutions already.

8. Cryptocurrencies

Best for: Risk-tolerant expats seeking high-reward upside and exposure to digital assets in a regulated environment.

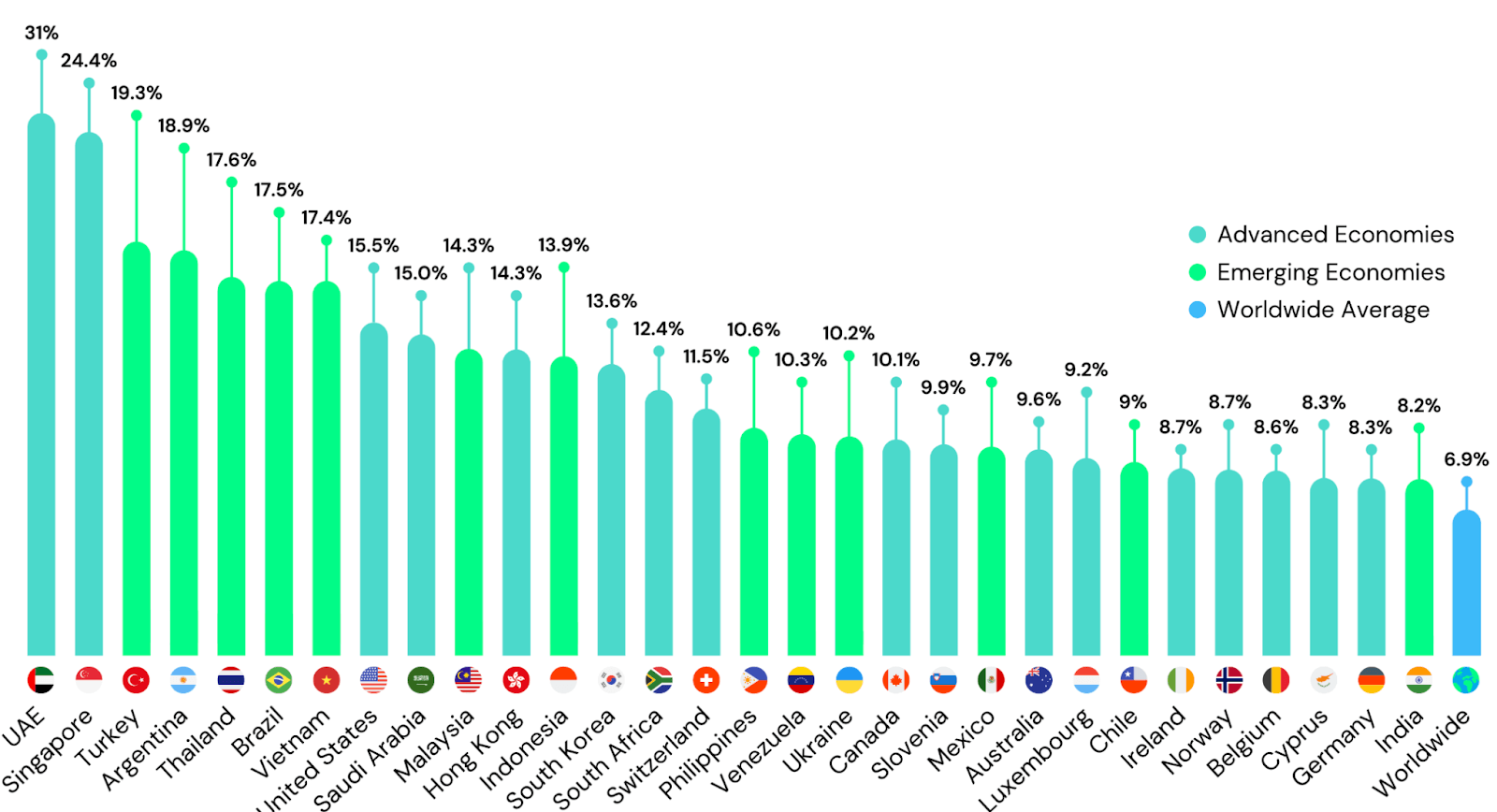

There are over 560 million cryptocurrency owners worldwide, out of which 31% live in the UAE.

Crypto remains a high-risk, high-reward investment, and the UAE is fast becoming one of the world's most regulated crypto hubs.

VARA in Dubai and DFSA in DIFC have built frameworks to license exchanges, enforce compliance, and protect investors.

Where can expats invest?

- BitOasis (local): Offers major coins like Bitcoin and Ethereum, with VARA oversight.

- MidChains (ADGM) and Rain (Bahrain-based) also serve UAE residents.

- Binance and Coinbase (global): Binance holds a full VARA operational license in Dubai (upgraded from MVP in 2024). Coinbase obtained a VARA license for institutional services but doesn't yet serve UAE retail customers.

- eToro: Regulated by ADGM/FSRA in the UAE (and top-tier authorities globally: FCA, CySEC, ASIC). Supports AED deposits via Online Banking / Instant Bank Transfer (~0.75% FX) or cards / bank wire (~8.2% FX) - pick the Online Banking method to minimise conversion costs.

- Sarwa: Regulated by FSRA, crypto trading (Bitcoin, Ethereum,...) is subject to a 0.75% spread.

Investment options include:

- Buying coins like Bitcoin or Ethereum for long-term appreciation

- Staking (e.g., ETH ~4% APY) or lending stablecoins to earn yield

- ETFs or regulated crypto funds via Swissquote or similar platforms

Risks: Volatility in crypto is extreme. Bitcoin has gained over 100% in some years and lost 80% in others. Other smaller tokens can go to zero in no time. We suggest you stick to licensed platforms, avoid shady yield schemes, and use proper security like 2FA or hardware wallets.

For expats, crypto offers exposure to a new asset class, no capital gains tax, and flexible access via global or local exchanges. But it’s not core portfolio material; limit exposure to 5% or less unless you’re deeply informed and willing to stomach big swings.

Also read: A guide to the best crypto exchanges in the UAE and Dubai

9. Startups and private equity

Best for: High-net-worth expats aiming for outsized returns by backing innovation and early-stage ventures.

Expats with higher risk tolerance can explore UAE-based startup and private equity opportunities, many of which operate under the regulatory umbrellas of DIFC and ADGM. These investments are illiquid and long-term, but if successful, they can offer exceptional returns.

Accessible options include:

- Equity crowdfunding platforms like Eureeca, DFSA-licensed and ADGM-regulated, let you invest in early-stage startups from just $100. You get shares and upside potential if the startup grows or exits. But exits can take years, and failure is common.

- Angel networks like Dubai Angel Investors are suited for those with more capital and time to vet deals, often starting from $5,000 per investment.

- Venture capital and private equity funds are meant for high-net-worth expats, in which VC pools investor capital into curated portfolios. These require large minimums but offer diversification and professional management.

Startup investing isn’t for everyone, but for expats seeking a high-risk, high-reward play, it offers a way to back innovation and take part in the region’s growth.

How to select the right investments as an Expat

With so many investment options available, choosing the right one comes down to understanding your personal goals, risk appetite, and long-term plans.

1. Start with your goals

Are you looking for income now? Maybe, to supplement your salary or support your family? Or are you planning for growth over time for retirement or a major future expense?

Income-focused investors tend to lean toward rental property, dividend stocks, or bonds. Growth-focused investors prefer global equities or startup investments.

In most cases, you will need a blend of both, depending on their stage of life and financial needs.

2. Assess your risk tolerance and time horizon

If market swings keep you up at night, steer clear of volatile assets like crypto or individual stocks. If you have a long investment horizon, say, 10+ years, you can usually afford more risk because you have time to recover.

For short-term goals (like buying a home in two years), capital preservation is more important, so savings accounts or short-term bonds are safer.

3. Understand tax and repatriation implications

The UAE has no income or capital gains tax, but your home country might. US citizens are taxed globally, and UK expats become taxable again upon returning.

Always plan ahead; a good practice is to sell taxable assets while in the UAE to lock in gains tax-free. When repatriating profits, keep records to prove origin and avoid delays or legal issues.

4. Diversify currency exposure

The AED is pegged to the USD, so holding assets in either is stable. But if your future expenses are in GBP, EUR, INR, or another home currency, consider shifting part of your portfolio accordingly.

Many banks and platforms allow multi-currency investing, helping you avoid being caught off guard by exchange rate movements later.

Risks and mistakes to avoid

Even seasoned investors make mistakes. And being an expat includes facing a few extra pitfalls. To keep your financial journey smooth, be aware of these common mistakes and risks:

- Overconcentration in real estate: It’s tempting to pour a huge chunk of your savings into UAE property, especially given the allure of rental income and the ‘tangibility’ of real estate. But putting too much in one asset class (or one property) is risky. Real estate is illiquid and subject to market cycles; a downturn (like the 2014-2018 softening in Dubai prices) could lock in your capital with no growth or even a loss, and you can’t easily sell.

- Unregulated investment schemes: Unfortunately, expat communities are often targeted by dubious investment schemes, from Ponzi schemes to get-rich-quick trading programs. Always verify that any investment provider or advisor is properly licensed (by SCA, DFSA, ADGM’s FSRA, or the Insurance Authority for life products). Check our Broker Warning List if you’re unsure.

- Not hedging against currency risk: Ignoring currency risks can hurt your portfolio. You might happily invest in USD/AED assets, but if you end up spending in another currency, exchange rates can affect your real returns.

- Lack of liquidity planning: Life is unpredictable. Being an expat, your job situation and plans can change quickly. A major mistake to avoid at all costs is tying too much of your money to illiquid or long-term investments without keeping enough accessible cash. Always maintain an emergency fund (3 to 6 months of expenses in your savings account).

Diversifying your capital across different asset classes (stocks, bonds, real estate, etc.), sectors, and regions reduces the impact of a downturn in any single asset, making your portfolio more resilient.

💡 Example: During the 2008 financial crisis, investors who held all their money in stocks lost more than those who had diversified into bonds, global ETFs, and real estate. Diversification helps spread risk.

Final thoughts

The UAE gives expats a rare edge: zero taxes, global access, and powerful local investment options. Whether it’s property, ETFs, or digital gold, the key is to diversity, stay informed, and think long term.

Don’t chase trends, build steadily. Start small if needed, but it's important to start. Your future wealth won’t build itself.

So invest smart, invest early, and let time do the heavy lifting.

Want to learn more? Read our guides on "how to invest money in the UAE" and “A Beginner's Guide to Personal Finance in the UAE”.

Explore our free calculators as well: