Best high-yield savings accounts in Dubai & the UAE (brokers & banks)

In the United Arab Emirates (UAE), banks offer a wide range of savings accounts tailored to meet the needs of residents and expatriates. You will find savings accounts both in AED and USD, including Sharia-compliant savings accounts.

In this article, we will explore the top savings accounts offered by brokers and traditional banks in the UAE, analyzing their interest rates, minimum and maximum balance requirements, eligibility criteria, and other essential features.

Quick comparison table

| Platform/account | Interest rate (AED/USD) | Min/max Balance | Main benefit |

|---|---|---|---|

| Mashreq NEO Plus Saver | Up to 6.25% (AED) | AED 50k (max 500k) | Top yield + cashback |

| ADCB Super Saver | Up to 4.50% (AED) | AED 50k | Bonus rate for new customers |

| Wio | Up to 4.00% (AED) | Salary ≥ AED 15k | Salary-linked high interest |

| FAB iSave | 4.00% (AED) – promotion | None | No withdrawal limits |

| Sarwa Save | 3.7% (USD) | None | Flexible & Sharia option |

| Trading 212 | 3.3% (USD) | None | Unlimited withdrawals |

| eToro | Up to 3.55% (USD) | None | Instant withdrawals |

| Interactive Brokers | 2.818% (AED); 3.14% (USD) | AED 35k / USD 10k | Brokerage-linked savings |

Note: All interest rates are annualized for USD and AED deposits and can change with market conditions. Always check if a rate is promotional (temporary) or requires a premium plan. Explore the companies mentioned and decide by yourself!

Top picks for different needs

- Highest AED Interest Rate: Mashreq NEO Plus Saver - Up to 6.25 % p.a. when you transfer a monthly salary of ≥AED 10k (5% if you simply keep ≥ AED 50k on deposit).

- Most Flexible AED Account (No Minimum, Unlimited Access): FAB iSave. The current promotion pays 4.00% p.a. on any balance - no hurdles, no lock-ins, and unlimited withdrawals.

- Best USD Yield: Sarwa. Perfect for expats or investors who already hold USD and want interest without sacrificing liquidity. New users can earn a signup bonus with the code RLLAA29D.

- Best Sharia-Compliant Option: Sarwa Save Halal. An expected return around 4.0% p.a. through Islamic money-market funds, zero minimum balance, and fully regulated by ADGM’s FSRA.

Tip: Because the UAE dirham is pegged to the US dollar, holding USD in broker platforms (eToro, Sarwa, IBKR) carries minimal FX risk for day-to-day spend in AED - but not zero.

Depth dive on the savings accounts in the UAE

Mashreq (NEO Plus Saver)

- Interest rate: Up to 6.25% (AED)

- Min/Max balance: AED 50,000 (max AED 500,000)

- Eligibility: UAE residents with Emirates ID; salary transfer or balance requirement

- Main benefit: Top yield + cashback

Mashreq Bank, one of the UAE’s oldest and fastest-growing digital banks, launched the NEO Plus Saver savings product in mid‑2025. Targeting both salaried and non‑salaried customers, it offers a 6.25% p.a. interest for those transferring a monthly salary of AED 10,000 or more via Mashreq NEO, plus up to AED 5,000 in initial cashback bonuses.

Customers who can’t transfer their salary can still earn 5% p.a. interest by maintaining a minimum balance of AED 50,000. Withdrawals are flexible (up to two free debits per month without losing interest), and interest is paid monthly on balances up to AED 500,000.

The entire account opening process is fully digital via the Mashreq Mobile App, providing access to fee‑free US stock trading, mutual funds, bonds, and more

How to start earning interest?

- Step 1: Open a Mashreq NEO Account, if you don’t have one.

- Step 2: Once your account is activated, open a NEO PLUS Saver Account through Mashreq Mobile App instantly.

- Step 3: Transfer your salary (at least AED 10,000) to Mashreq NEO or keep balance of at least AED 50,000.

- Step 4: Move money from your NEO Account to your NEO PLUS Saver Account to start earning interest.

Mashreq Bank PSC is fully regulated and licensed by the UAE Central Bank (formerly CBUAE), operating under its banking supervision and licensing framework.

ADCB (Super Saver)

- Interest rate: Up to 4.5% (AED)

- Min/Max balance: AED 50,000

- Eligibility: UAE residents; new customers preferred

- Main benefit: Bonus rate for new customers

ADCB (Abu Dhabi Commercial Bank) is one of the UAE’s leading banks, known for its strong digital services and customer-focused offerings.

The Super Saver Account provides up to 4.5% p.a. interest (including a promotional bonus for new customers) for balances starting at AED 50,000. The account features monthly interest payouts, seamless digital onboarding, and is ideal for UAE residents seeking competitive savings rates from a well-established, fully regulated bank.

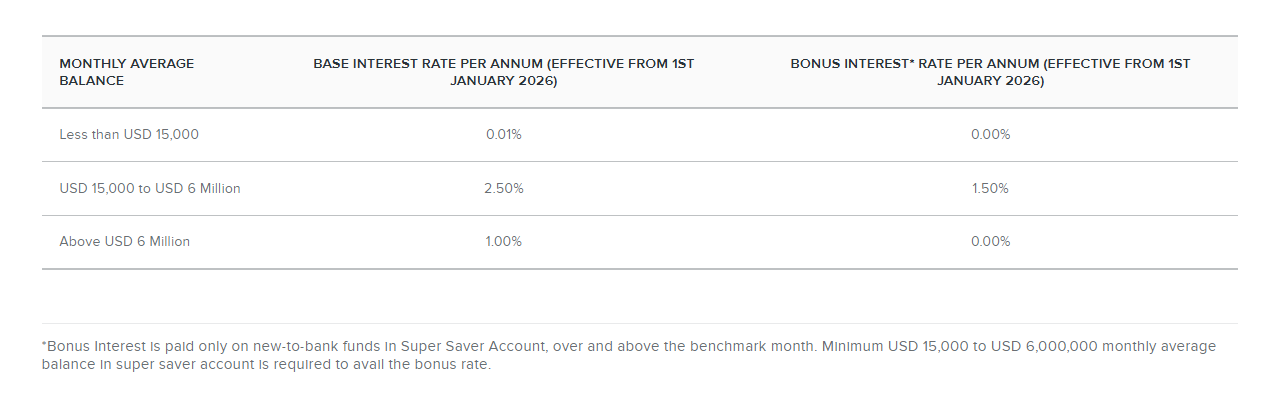

After the promotion, these are the base rates (AED):

In USD:

ADCB (Abu Dhabi Commercial Bank PJSC) is fully licensed and regulated by the Central Bank of the United Arab Emirates (CBUAE), which oversees all conventional and Islamic banks operating onshore in the UAE

Wio (Digital Bank – Emirates NBD)

- Interest rate: Up to 4.00% (AED)

- Min/Max balance: Salary ≥ AED 15,000

- Eligibility: UAE residents with Emirates ID

- Main benefit: Salary-linked high interest

Wio Bank PJSC is the first fully licensed digital-native bank in the UAE, backed by Abu Dhabi government entity ADQ (65%), Etisalat (25%), and First Abu Dhabi Bank (10%). Launched in 2022, it offers app-based personal and business banking tailored to UAE residents.

Its Salary Plan allows eligible customers (transferring salary ≥ AED 15,000 within two months) to access up to 6% p.a. interest on savings (up to AED 1M), 3% p.a. on current account balances, and up to 2% cashback on card spends. Withdrawals and transfers remain flexible and digital-first.

The 6% interest rate (Expressed annually) is only applicable for 1 month, that’s why we did not give too much focus on that (decided to highlight the 4.00%):

.png)

Wio Bank is fully licensed and regulated by the Central Bank of the UAE, adhering to consumer protection standards, financial integrity rules, and security provisions set by the CBUAE

FAB (iSave)

- Interest rate: 4.00% (AED) – promotion till June 30, 2026

- Min/Max balance: None

- Eligibility: UAE residents

- Main benefit: No withdrawal limits

.png)

FAB, formed in 2017 through the merger of First Gulf Bank and National Bank of Abu Dhabi, is the largest bank in the UAE by assets and is widely recognized for its digital banking excellence.

The iSave Account is an online-only savings account offering a promotional interest rate of up to 4.00% p.a. on new funds deposited until at least June 30, 2026, with no minimum balance requirement and unlimited withdrawals.

FAB is fully licensed and regulated by the Central Bank of the UAE (CBUAE), which oversees its compliance with banking laws, capital adequacy, consumer protection, and financial crime standards.

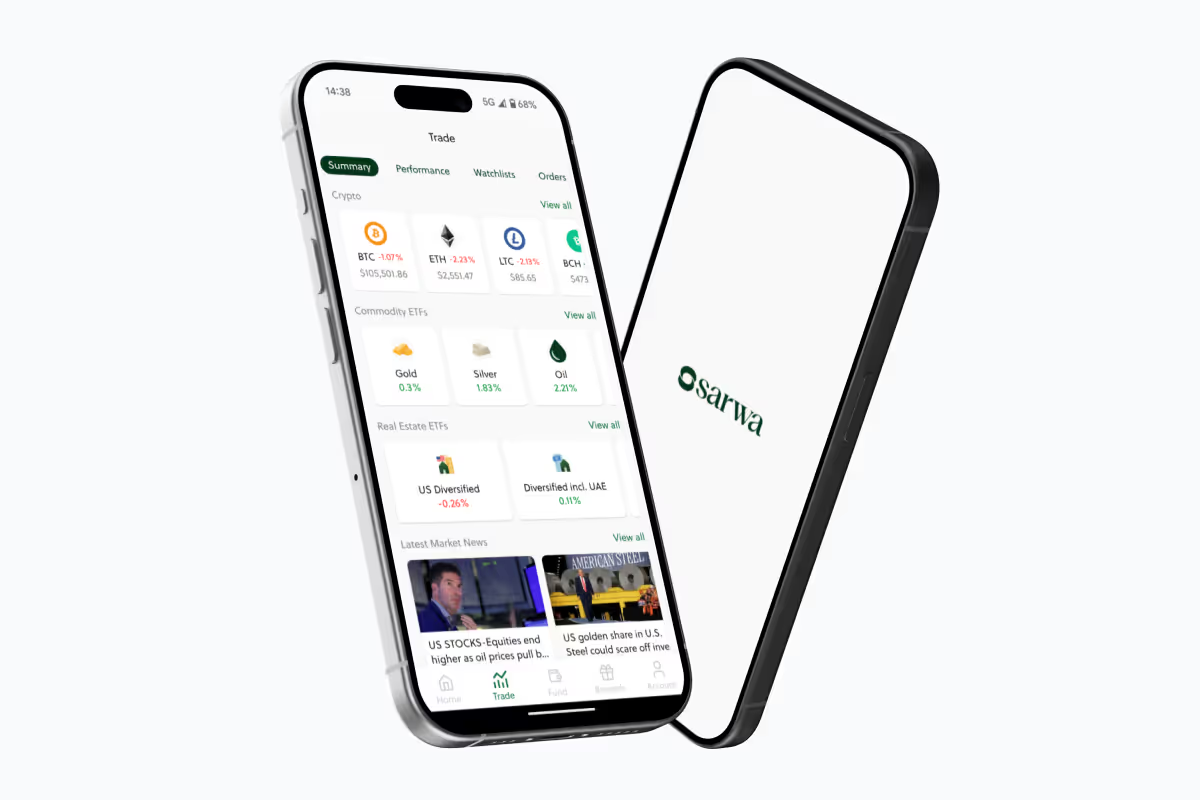

Sarwa (Sarwa Save)

- Interest rate: 3.7% (USD)

- Min/Max balance: None

- Eligibility: UAE residents (via Sarwa app)

- Main benefit: Flexible & Sharia option

.png)

Sarwa Digital Wealth (Capital) Limited is a UAE‑based fintech platform (founded in 2017, headquartered in Abu Dhabi) offering a suite of financial services, including Sarwa Save which provides a cash‑management fund offering estimated returns (e.g., 3.7% for Save+ or 4.0% for Halal variant), with no lock‑in, no minimum balance, and zero withdrawal fees.

.png)

Sarwa Digital Wealth (Capital) Limited is regulated by the Financial Services Regulatory Authority (FSRA) of the Abu Dhabi Global Markets (ADGM) under a Category 3C licence that covers retail and investment money activities.

Although Sarwa isn’t a bank, client funds are held with reputable custodian banks, such as Saxo Bank (Denmark), regulated by the Danish financial authority, as well as BMO Harris in connection with trade and custody operations. These custodians keep client assets segregated from Sarwa’s own corporate accounts.

Trading 212

- Interest rate: 3.3% (USD)

- Min/Max balance: None

- Eligibility: Open to UAE residents via global platform

- Main benefit: Unlimited withdrawals

.png)

Trading 212 is a UK-based fintech brokerage founded in 2004, offering commission‑free trading in stocks, ETFs, and CFDs, along with fractional shares and automated portfolio tools like “Pies” and AutoInvest.

You also have access to a debit card, cashback on your spending and interest in several currencies. Unfortunately, AED is not one of them.

In the UAE, Trading 212 operates under the subsidiary “Trading 212 UK Ltd”, regulated by the UK’s Financial Conduct Authority (FCA), offering compensation of up to £85,000 via the Financial Services Compensation Scheme (FSCS).

Want to know more? Check our in-depth Trading 212 review.

eToro

- Interest rate: Up to 3.55% (USD)

- Min/Max balance: None

- Eligibility: Available globally, UAE residents included

- Main benefit: Instant withdrawals

.png)

eToro is a global multi‑asset investment platform founded in 2007, with over 30 million users worldwide. It offers commission‑free trading for ETFs and low commissions on cryptocurrencies, CFDs, forex, indices, and commodities (supports fractional shares).

eToro allows you to earn interest on uninvested USD balances, giving you passive earnings directly in your account with monthly payments (Interest is paid into your eToro balance every month) and no lock-in (funds remain fully liquid; withdraw at any time).

The interest is paid according to your balance. The lowest interest you can get is 1% on USD and the highest is 3.55%:

.png)

eToro is available in the UAE through eToro (ME) Limited, regulated by ADGM’s FSRA.

eToro also offers welcome bonuses for UAE users.

Want to know more? Check our in-depth eToro review.

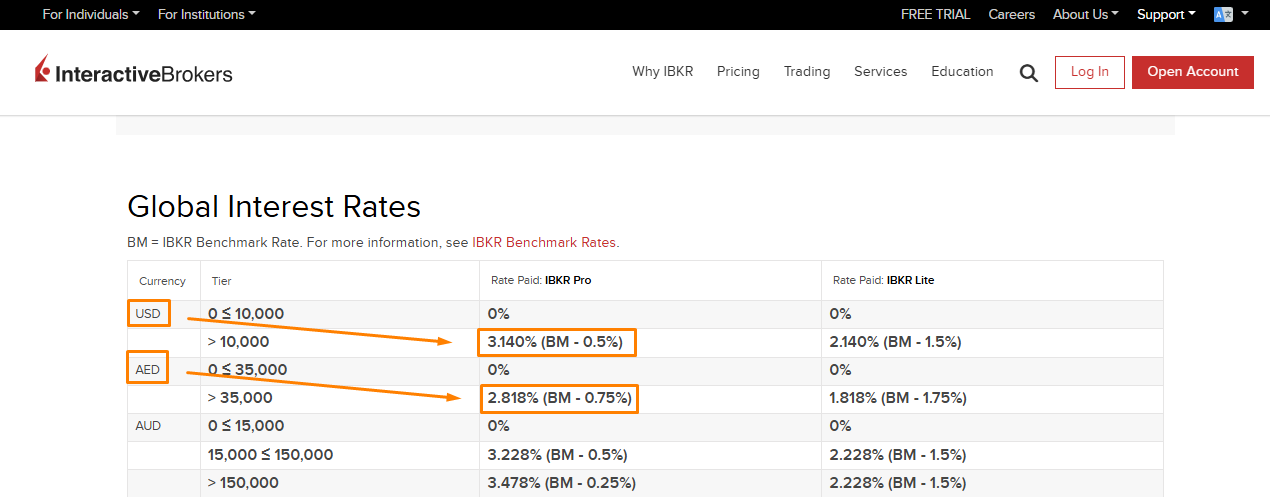

Interactive Brokers (IBKR)

- Interest rate: 2.818% (AED); 3.14% (USD)

- Min/Max balance: AED 35,000 / USD 10,000

- Eligibility: Available globally, UAE residents included

- Main benefit: Brokerage-linked savings

Interactive Brokers Group, Inc. is a U.S.-based multinational brokerage founded in 1978, headquartered in Greenwich, Connecticut. It serves over 3.3 million clients worldwide, offering direct-access trading across equities, options, futures, forex, bonds, ETFs, CFDs, crypto, and more.

Interest is tier-based, payable only for idle balances above minimum thresholds:

- USD: no interest on first USD 10,000; balances above earn up to 3.14% (IBKR Pro)

- AED: no interest on first AED 35,000; above that, 2.818% (IBKR Pro)

Eligibility requires an account NAV equivalent to at least USD 10,000; the maximum rate typically achieved at USD 100,000+ NAV.

The entity operating locally is Interactive Brokers (U.K.) Limited – DIFC Branch, which is regulated by the Dubai Financial Services Authority (DFSA) under DFSA register F008423, authorised to arrange deals in investments and custody within DIFC.

Want to know more? Check our Interactive Brokers review.

Overview of the UAE savings market

The UAE savings market continues to be shaped by a combination of macroeconomic conditions and competitive deposit rate offerings, which are largely influenced by the Central Bank of the UAE (CBUAE) base rate and the Emirates Interbank Offered Rate (EIBOR).

Interest rate environment

- CBUAE Base Rate: As of mid-2026, the CBUAE base rate has remained stable at 3.65%, closely tracking the U.S. Federal Reserve’s policy rate due to the UAE dirham’s peg to the U.S. dollar.

- EIBOR: Short-term EIBOR (typically the 3-month tenor) is also hovering near 3.5%, reflecting the interbank funding costs that drive pricing for savings and deposit products.

- Savings Yields: Retail deposit rates in the UAE generally range between 3.5% and 6% per annum, with the upper end of this range often tied to promotional campaigns or specific balance tiers.

This alignment between the CBUAE base rate and EIBOR creates a highly competitive environment for depositors, as financial institutions adjust their rates to attract liquidity while maintaining healthy net interest margins.

UAE retail investor landscape

- High savings propensity: According to a recent market survey, nearly half (48%) of investors have been saving by building up a balance of money in their bank account over the past 12 months, with savings accounts and fixed deposits remaining the most popular vehicles.

- Preference for liquidity: A significant portion of UAE retail investors demonstrate short holding periods: 33% hold investments for months, 22% for weeks, and 7% for days, implying a substantial inclination toward liquid or cash-equivalent investment behavior rather than long-term vehicles

- Response to rates: Retail investors have shown high sensitivity to changes in interest rates, with deposit inflows increasing significantly when rates exceed the 4% threshold, closely tied to the CBUAE base rate and EIBOR movements.

Banks vs. Brokers: Key differences

In the UAE, savings products are offered by two main types of institutions: traditional banks and brokerage or fintech platforms. Understanding the distinction is crucial:

| Feature | Banks | Brokers/Fintech |

|---|---|---|

| Regulator | Central Bank of the UAE (CBUAE) | FSRA (ADGM), DFSA (DIFC), FCA (UK) |

| Deposit Protection | Local regulatory oversight (no explicit deposit insurance like FDIC, but CBUAE monitoring) | No UAE deposit protection; relies on custodian arrangements or international schemes (e.g. FSCS in the UK) |

| Currency Options | Mainly AED and USD | Primarily USD; some offer AED (e.g. Interactive Brokers) |

| Access | Requires Emirates ID and residency | Often available globally; some accept UAE residents without Emirates ID |

| Liquidity | Free withdrawals (some with monthly limits) | Full liquidity; usually no withdrawal penalties |

| Extra Benefits | Salary-linked perks, cashback, local ATM network | Trading features, higher USD rates, global diversification |

When to choose a bank: If you need AED savings, local salary transfer features, or want a purely regulated UAE banking product.

When to choose a broker: If you hold USD savings, want higher flexibility, or combine investing with savings.

Eligibility for non-residents and expatriates

Eligibility varies significantly depending on the platform:

Banks

- Emirates ID required: Most banks (e.g. Mashreq, ADCB, FAB, Wio) require UAE residency.

- Salary transfer: Some banks (e.g. Mashreq NEO Plus Saver, Wio Salary Account) require a monthly salary transfer to unlock the highest rates.

- Promotions for new customers: Certain rates (e.g. ADCB Super Saver bonus) are only for first-time account holders.

Brokers

- Available globally: Platforms like Interactive Brokers, eToro, and Trading 212 allow UAE residents to open accounts online without needing a UAE salary transfer.

- Expat-friendly: Sarwa Save (regulated in ADGM) is specifically designed for UAE residents, including expatriates, and has no minimum deposit requirement.

- Non-residents: Some brokers accept clients from outside the UAE, but interest in AED is usually unavailable; USD is the default.

Risks and safety considerations

When choosing between banks and brokers, safety is a top priority. Here’s how each is regulated and how your money is protected:

Banks (CBUAE)

- Licensed and supervised by the Central Bank of the UAE (CBUAE).

- Capital adequacy requirements ensure banks maintain sufficient reserves.

- While the UAE does not have a formal deposit insurance scheme, the CBUAE has a strong track record of supporting banks during financial stress.

- Banks also follow strict anti-money laundering (AML) and consumer protection rules.

Brokers

- ADGM (FSRA) or DIFC (DFSA) regulation applies to local UAE branches (e.g. Sarwa, Interactive Brokers DIFC).

- International protections may apply for foreign entities:

- Trading 212 UK: Covered by the UK’s FSCS, which protects up to GBP 85,000.

- Interactive Brokers: Uses segregated custodial accounts and is regulated in multiple jurisdictions.

- Custodian banks (e.g. Sarwa uses Saxo Bank in Denmark and BMO Harris in the U.S.) keep client funds separate from company operating accounts.

Currency risk

If you save in USD but your expenses are in AED, exchange rate changes can impact your effective return. However, because the AED is pegged to the USD, this risk is very low but not entirely zero.

Sharia-compliant savings accounts

For those seeking faith-based financial products, Sharia-compliant savings accounts are a growing segment in the UAE. These accounts follow Islamic finance principles: no interest (riba) is paid. Instead, profit-sharing or other Sharia-compliant structures are used.

Examples:

- Sarwa Save Halal:

- Regulated by FSRA in ADGM.

- Provides a Sharia-compliant alternative to its USD cash product (around 4.0% expected return).

- Uses Islamic money market funds that comply with Sharia rules.

- Emirates Islamic and ADIB:

- Offer profit-bearing savings accounts (AED and USD) where returns come from Islamic financing contracts (e.g. mudarabah).

- Fully regulated by CBUAE.

Bottom line

Saving money in the UAE has never been more rewarding, with options ranging from traditional banks offering competitive AED interest rates to brokerage platforms providing flexible USD-based returns.

Choose based on your income currency, residency status, risk tolerance, and liquidity needs. While banks provide local security and AED-based stability, brokers offer higher USD returns and global accessibility. A blended approach can be the most effective strategy in 2026.